It’s finally 2024 and everyone wants to know what’s going to happen to the real estate market in the coming year! Will prices go up? Will we start to see more listings? Will I finally be able to afford a home in the foothills? All great questions! But before we can look forward to what’s likely to happen to the market in 2024, we need to look back and understand what happened in 2023. The data for 2023 is fascinating and it can give us both context and a better chance of correctly predicting what’s likely to come in 2024.

In 2023, across the foothills market, it was both more difficult to buy and more difficult to sell a house than it has been in decades. Inventory remained extremely low, days on market increased, the quality of listings decreased, and affordability hit new lows – creating a perfect storm for the lowest number of transactions we’ve seen in a long time. What caused the market to behave this way? Well, if the housing market in 2021-2022 was defined by the effects of the pandemic and the rise of work-from-home (buyers seeking to get out of the city and needing more space), 2023 was defined by the effects of interest rates!

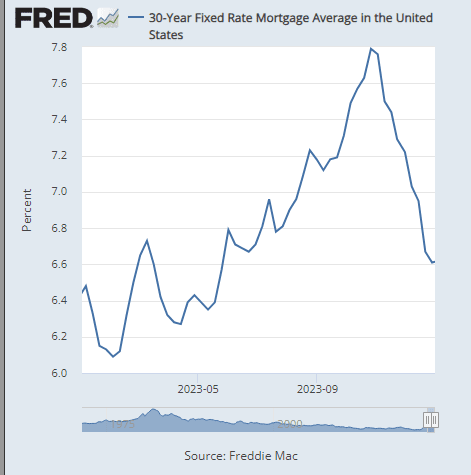

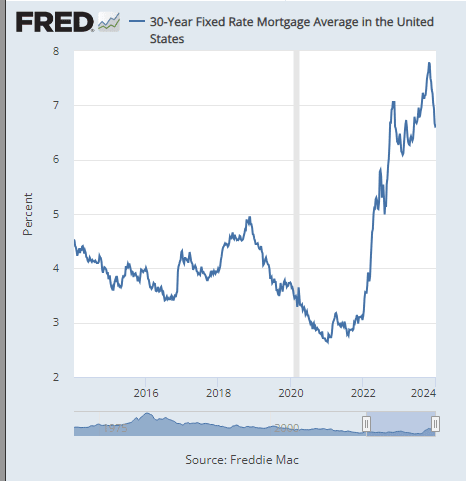

Look at the following charts, the 30-year mortgage rate through 2023 compared to the last ten years:

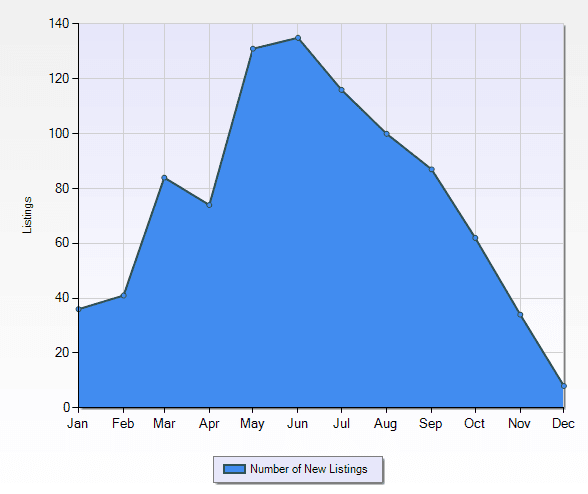

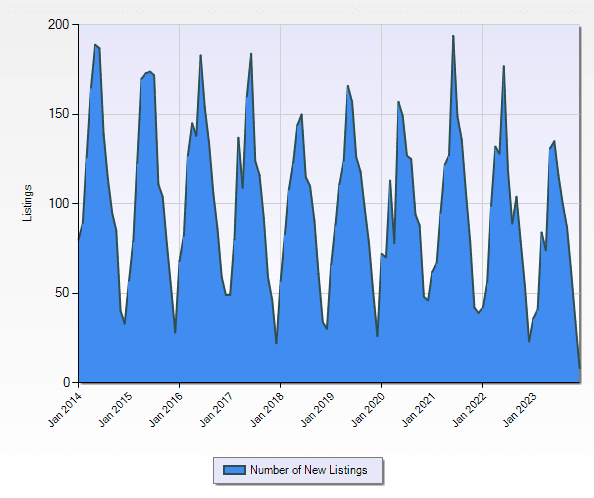

Rates spiked dramatically since the beginning of 2022 from pandemic lows near 2.75% to a high of over 8% in our market in September 2023. This increased the principal and interest on a $600,000 mortgage from about $2,450 to over $4,500 – a nearly 84% increase in monthly payment for the same loan amount! Now, historically, as anyone in their 60s or 70s will tell you, 8%’s not that bad (“my first mortgage was 14% [grumble, grumble”). But it sure seemed bad to those who were thinking about buying a house with a mortgage in 2023. On the flip side, sellers who all refinanced to market lows of 3% or below were reluctant to give up their mortgages, buy something new, and nearly double their monthly payments. So, they didn’t list their homes for sale, happy to age in place, rent their home out, or just stay where they’re at and work from home. Look at the data for new listings in 2023 (particularly in the fourth quarter after rates spiked) compared to the prior ten years:

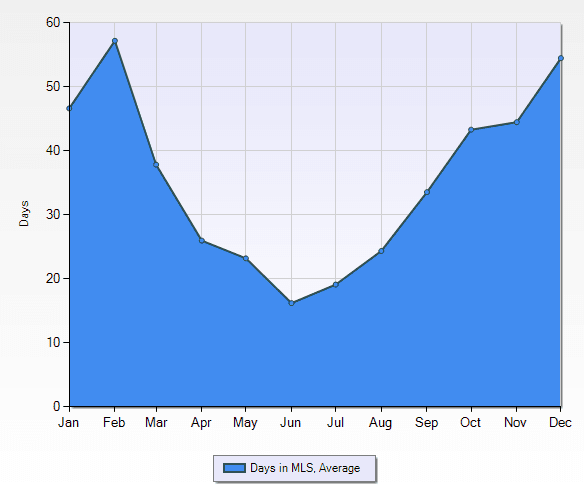

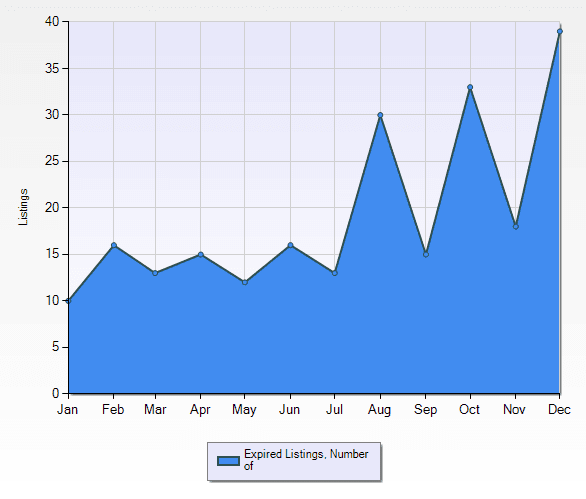

Add to that, increasing days on market and a dramatic increase in listings not selling and expiring:

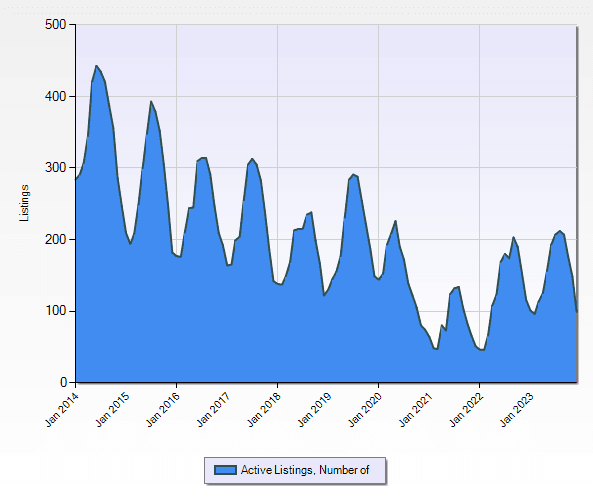

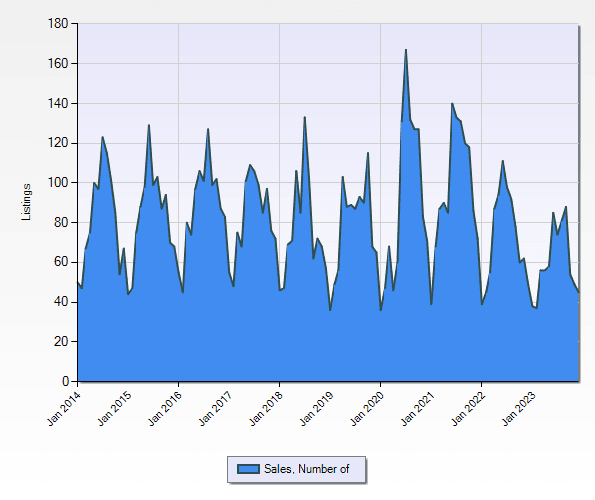

And, you get, near decade (non-pandemic) lows in active listings and sales:

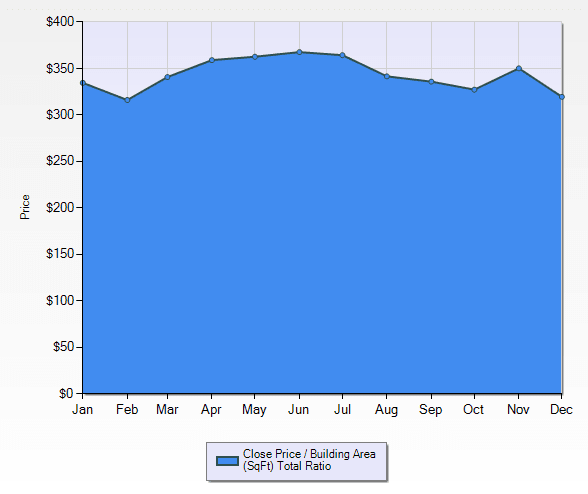

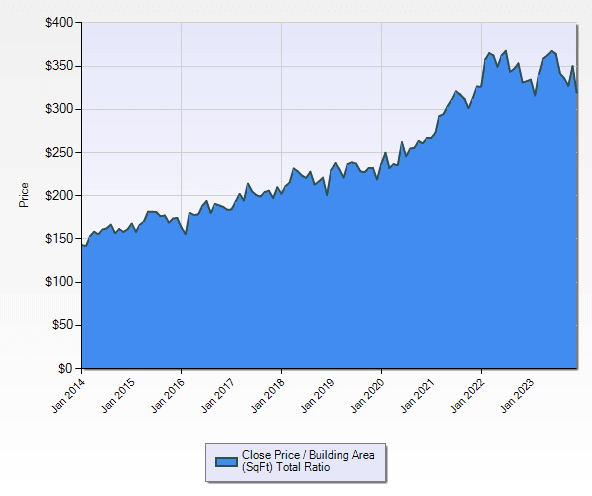

Long story short, inventory was low, buyer activity was low, and listings took a long time to sell, particularly towards the end of the year when rates peaked. The market in most segments was simply frozen and as a result, prices were pretty stable and close to where you would expect them to be based on the long-term appreciation trend:

Regardless, people still need to sell homes! Homeowners still sometimes need to move for work, downsize, get divorced, die, or have other life events that make them want to move. And buyers still desperately want to buy. Potential buyers want to get out of the city, they have kids, they outgrow their apartments, they want smaller homes or larger homes than they have currently, or they move to town for work, lifestyle, or family. So where were all the transactions? Simply put – sellers and buyers are both waiting. But for what? And until when? The answer is the key to understanding the 2024 market.

Denver Foothills Property, powered by Compass, is your trusted partner in navigating the unique real estate opportunities of Colorado’s Foothills. From luxury homes to sprawling estates and land, we bring expertise, dedication, and an unmatched understanding of the market. Contact us today to start your real estate journey.

Nick Melzer, JD, founder of Denver Foothills Property, is a seasoned Realtor®, licensed attorney, and the top land broker in Colorado’s Foothills market. Specializing in luxury homes, estates, and land, Nick brings a unique skill set to every transaction, ensuring a seamless and successful experience for his clients.

Social Cookies

Social Cookies are used to enable you to share pages and content you find interesting throughout the website through third-party social networking or other websites (including, potentially for advertising purposes related to social networking).